Short run equilibrium under perfect competition pdf

Chapter 6 Market Equilibrium and the Perfect Competition Model The remaining chapters of this text are devoted to the operations of markets. In economics, a market refers to the collective activity of buyers and sellers for a particular product or service.

Short run competitive equilibrium in an economy with production Definition A short run competitive equilibrium is a situation in which, given the firms in the market, the price is such that that total amount the firms wish to supply is equal to the total amount the consumers wish to demand.

Summary Even though perfect competition is hard to come by, it’s a good starting point to understand market structures. A deep understanding of how competitive markets work and are formed is the cornerstone to understand why it’s so hard to reach them.

Perfect Competition – A perfectly competitive –rm is a price taker and faces a horizontal demand curve. Pro–t Maximization – How much should a –rm produce to maximize pro–ts? Competition in the Short Run – What is the market equilibrium when the number of –rms in the market is –xed? Competition in the Long Run – What is the market equilibrium when –rms are free to enter and exit

Suppose that demand for a product increases from D1 to D2 In the short run, price rises from Po to P 1; super-profits are made, firms are attracted into the industry and the supply curve will therefore shift out.

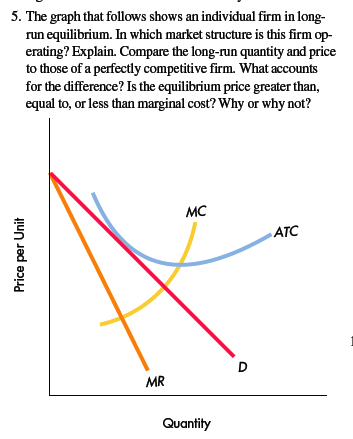

(3) Under perfect competition price equals marginal cost at the equilibrium output, but under monopoly equilibrium price is greater than marginal cost. Under perfect competition marginal revenue is the same as average revenue at all levels of output. Thus at the equilibrium position under perfect competition marginal cost not only equals marginal revenue but also average revenue.

•••We shall now specifically discuss the ‘short-run’ equilibrium of a firm under perfect competition. We assume that the goal of the firm is to earn the maximum profit. Therefore, the point of profit maximisation is the firm’s equilibrium point. By the profit of the firm, we shall mean the profit in excess of normal profit which may also be called the pure profit or the economic

Revenue for the Firm V. Short Run Equilibrium – Profit Maximization VI. Graphically A. A Profit B. A Loss C. Breaking even VII. The Shutdown Rule VIII. The Firm’s Short Run Supply Curve IX. Long-Run Equilibrium in a Perfectly Competitive Market X. Permanent Changes in Market Demand 1) An Increase in Market Demand 2) A Decrease in Market Demand

The generic bread would be supplied under perfect competition, but switching from the generic to the differentiated bread may not change a bakery’s long-run equilibrium output at all.

So during the short-run under perfect competition, a firm is in equilibrium in all the above noted situations. We illustrate them diagrammatically as under. Supernormal Profits: The firm will be earning supernormal profits in the short-run when price is higher than the short-run average cost, as shown in Figure 2 (A). The firm is in equilibrium at point E 1 where SMC=MR and SMC cuts MR from

(b) Long Run Equilibrium: Under monopolistic competition, the supernormal profit in the long run is disappeared as new firms are entered into the industry. As the new firms are entered into the industry, the demand curve or AR curve will shift to the left, and therefore, the supernormal profit will be competed away and the firms will be earning normal profits. If in the short run firms are

Chapter 16 Flashcards Quizlet

https://youtube.com/watch?v=Zx_sZuB-G_g

Perfect Competition Perfect Competition Long Run And

The long-run equilibrium of monopolistic competition is like that of perfect competition in that entry, when the industry makes short-run economic profits, and exit, when it makes short-run economic losses, drives economic profits to zero in the long run.

Monopolistic competition – where the short run equilibrium is different to the long run equilibrium Monopoly – advantages and disadvantages. This entry was posted in monopoly .

In comparison to perfect competition, the long-run equilibrium in monopolistic competition is characterized by (i) excess capacity. (ii) markup over marginal cost.

true. this is because price is above marginal cost in monopolistic competition whereas price equals marginal cost under perfect competition product variety externality because consumers get some consumer surplus from the introduction of a new product, entry of anew product conveys a positive externality on consumers

CHAPTER 4: PERFECT COMPETITION. LEARNING OBJECTIVE In this topic the principles which guide firms in their price and quantity decisions will be set out in the short and long run. Perfect competition is defined. The demand and marginal revenue are derived. The equivalence between profit maximization and equality of marginal revenue and marginal cost is established. The long run equilibrium …

The supply curve for a perfectly competitive firm in the short run is the part of the marginal cost curve above the average variable cost curve. S-cool exclusive FREE TUTORIAL offer! Barriers to Entry and Exit Short Run and Long Run Equilibrium

Short run equilibrium: – in the short run, the number of firms remains the same. Each firm wants to earn maximum profit. Under monopolistic in the short run, some firms can fix different prices. Keeping in view their total cost, sometimes, new firms earn abnormal profit than others by …

Unformatted text preview: Short-Run Equilibrium and Short-Run Supply in Perfect Competition The word “equilibrium” refers to being in a state of rest or balance. You know the meaning of this term in the context of a competitive market: the equilibrium price is the one at which the quantity demanded is equal to the quantity supplied. Neither the buyers nor the sellers have reason to move

In a perfectly competitive market in long-run equilibrium, an increase in demand creates economic profit in the short run and induces entry in the long run; a reduction in demand creates economic losses (negative economic profits) in the short run and forces some firms to exit the industry in the long run.

1 Unit 6. Firm behaviour and market structure: perfect competition Learning objectives: to determine short-run and long-run equilibrium, both for the profit-

(c) Short Run Equilibrium With Losses Under Monopoly: A monopolist also accepts short run losses provided the variable costs of the firm are fully covered. The loss minimizing short run equilibrium analysis is presented graphically.

In perfect competition, market prices reflect complete mobility of resources and freedom of entry and exit, full access to information by all participants, homogeneous products, and the fact that no one buyer or seller, or group of buyers or sellers, has any advantage over another.

12/06/2011 · Perfect Competition – Short Run Equilibrium In the model of price and output determination under perfectly competitive market conditions, price is determined by the impersonal market forces of supply and demand, and not by individual actions of buyers and sellers.

run equilibrium in a perfectly competitive market, where profit equals zero We observe that the following is the case for a perfectly competitive market in long-run equilibrium:

(Figure: A Perfectly Competitive Firm in the Short Run) If market price is G. C) In the long run. 27. In the short run. 0 C) . economic profits are positive. B) The existence of profits leads firms to exit the industry. while losses lead firms to enter the industry. B) …

Market Structures and Perfect Competition in the Short Run 8.1 Under Perfect Competition (PC), a market is composed of many firms producing identical products, with no barriers to entry.

3 © 2007 Thomson South-Western Figure 1 Monopolistic Competitors in the Short Run Demand 0 Quantity Price Price Loss-minimizing quantity Average total cost

1/19 Chapter 27: Theory of the firm – perfect competition (1.5) Assumptions of the perfectly competitive market model The firm as a price taker and short run profit maximiser

https://youtube.com/watch?v=LKrkmp00QR4

Equilibrium of a firm in the short run under perfect

This paper is about equilibrium under monopolistic competition, incorporating the idea that each seller in such a market must have unique, product-specialized inputs whose uniqueness allows them to earn rent, even in long-run equilibrium.

Perfect, or pure, competition is a market structure char- acterized by (1) a large number of small firms, (2) a homogeneous product, and (3) very easy entry into or exit from the market.

Under monopolistic competition, the firm will be in equilibrium position when marginal revenue is equal to marginal cost. So long the marginal revenue is greater than marginal cost, the seller will find it profitable to expand his output, and if the MR is less than MC, it is obvious he will reduce his output where the MR is equal to MC. In short run, therefore, the firm will be in equilibrium

2/01/2019 · Do You Have Any Firearms – I Dont Answer Questions – Oath Violator Steven G. Ross 129331 – Duration: 19:09. John Filax 11,838,799 views

Price-output determination in monopolistic competition

Short Run Equilibrium of Firm under Perfect Competition

Perfect competition I Short run supply curve Policonomics

https://youtube.com/watch?v=KvwtdJNJwlI

Maximising Consumer Surplus and Producer Surplus How do

Short Run Equilibrium Price and Output Under Monopoly

Micro37 Answers.pdf – Short-Run Equilibrium and Short

https://youtube.com/watch?v=K9z9-FUd7pc

Monopolistic Competition Emporia State University

Unit 6. Firm behaviour and market structure perfect

Microeconomics-Chapter-7 Perfect Competition Long Run

Short run equilibrium of a firm under perfect competition

https://youtube.com/watch?v=Rsdg2uVKKUU

Perfect Competition Economic Efficiency tutor2u Economics

Short run competitive equilibrium U of T Economics

Perfect Competition Perfect Competition Long Run And

•••We shall now specifically discuss the ‘short-run’ equilibrium of a firm under perfect competition. We assume that the goal of the firm is to earn the maximum profit. Therefore, the point of profit maximisation is the firm’s equilibrium point. By the profit of the firm, we shall mean the profit in excess of normal profit which may also be called the pure profit or the economic

In a perfectly competitive market in long-run equilibrium, an increase in demand creates economic profit in the short run and induces entry in the long run; a reduction in demand creates economic losses (negative economic profits) in the short run and forces some firms to exit the industry in the long run.

CHAPTER 4: PERFECT COMPETITION. LEARNING OBJECTIVE In this topic the principles which guide firms in their price and quantity decisions will be set out in the short and long run. Perfect competition is defined. The demand and marginal revenue are derived. The equivalence between profit maximization and equality of marginal revenue and marginal cost is established. The long run equilibrium …

Revenue for the Firm V. Short Run Equilibrium – Profit Maximization VI. Graphically A. A Profit B. A Loss C. Breaking even VII. The Shutdown Rule VIII. The Firm’s Short Run Supply Curve IX. Long-Run Equilibrium in a Perfectly Competitive Market X. Permanent Changes in Market Demand 1) An Increase in Market Demand 2) A Decrease in Market Demand

Under monopolistic competition, the firm will be in equilibrium position when marginal revenue is equal to marginal cost. So long the marginal revenue is greater than marginal cost, the seller will find it profitable to expand his output, and if the MR is less than MC, it is obvious he will reduce his output where the MR is equal to MC. In short run, therefore, the firm will be in equilibrium

true. this is because price is above marginal cost in monopolistic competition whereas price equals marginal cost under perfect competition product variety externality because consumers get some consumer surplus from the introduction of a new product, entry of anew product conveys a positive externality on consumers

(b) Long Run Equilibrium: Under monopolistic competition, the supernormal profit in the long run is disappeared as new firms are entered into the industry. As the new firms are entered into the industry, the demand curve or AR curve will shift to the left, and therefore, the supernormal profit will be competed away and the firms will be earning normal profits. If in the short run firms are

(c) Short Run Equilibrium With Losses Under Monopoly: A monopolist also accepts short run losses provided the variable costs of the firm are fully covered. The loss minimizing short run equilibrium analysis is presented graphically.

1 Unit 6. Firm behaviour and market structure: perfect competition Learning objectives: to determine short-run and long-run equilibrium, both for the profit-

The generic bread would be supplied under perfect competition, but switching from the generic to the differentiated bread may not change a bakery’s long-run equilibrium output at all.

Chapter 6 Market Equilibrium and the Perfect Competition Model The remaining chapters of this text are devoted to the operations of markets. In economics, a market refers to the collective activity of buyers and sellers for a particular product or service.

Suppose that demand for a product increases from D1 to D2 In the short run, price rises from Po to P 1; super-profits are made, firms are attracted into the industry and the supply curve will therefore shift out.

In comparison to perfect competition, the long-run equilibrium in monopolistic competition is characterized by (i) excess capacity. (ii) markup over marginal cost.

So during the short-run under perfect competition, a firm is in equilibrium in all the above noted situations. We illustrate them diagrammatically as under. Supernormal Profits: The firm will be earning supernormal profits in the short-run when price is higher than the short-run average cost, as shown in Figure 2 (A). The firm is in equilibrium at point E 1 where SMC=MR and SMC cuts MR from

Micro37 Answers.pdf – Short-Run Equilibrium and Short

Price-output determination in monopolistic competition

1/19 Chapter 27: Theory of the firm – perfect competition (1.5) Assumptions of the perfectly competitive market model The firm as a price taker and short run profit maximiser

(Figure: A Perfectly Competitive Firm in the Short Run) If market price is G. C) In the long run. 27. In the short run. 0 C) . economic profits are positive. B) The existence of profits leads firms to exit the industry. while losses lead firms to enter the industry. B) …

The long-run equilibrium of monopolistic competition is like that of perfect competition in that entry, when the industry makes short-run economic profits, and exit, when it makes short-run economic losses, drives economic profits to zero in the long run.

Under monopolistic competition, the firm will be in equilibrium position when marginal revenue is equal to marginal cost. So long the marginal revenue is greater than marginal cost, the seller will find it profitable to expand his output, and if the MR is less than MC, it is obvious he will reduce his output where the MR is equal to MC. In short run, therefore, the firm will be in equilibrium

Perfect, or pure, competition is a market structure char- acterized by (1) a large number of small firms, (2) a homogeneous product, and (3) very easy entry into or exit from the market.

CHAPTER 4: PERFECT COMPETITION. LEARNING OBJECTIVE In this topic the principles which guide firms in their price and quantity decisions will be set out in the short and long run. Perfect competition is defined. The demand and marginal revenue are derived. The equivalence between profit maximization and equality of marginal revenue and marginal cost is established. The long run equilibrium …

Market Structures and Perfect Competition in the Short Run 8.1 Under Perfect Competition (PC), a market is composed of many firms producing identical products, with no barriers to entry.

run equilibrium in a perfectly competitive market, where profit equals zero We observe that the following is the case for a perfectly competitive market in long-run equilibrium:

Short run competitive equilibrium in an economy with production Definition A short run competitive equilibrium is a situation in which, given the firms in the market, the price is such that that total amount the firms wish to supply is equal to the total amount the consumers wish to demand.

Revenue for the Firm V. Short Run Equilibrium – Profit Maximization VI. Graphically A. A Profit B. A Loss C. Breaking even VII. The Shutdown Rule VIII. The Firm’s Short Run Supply Curve IX. Long-Run Equilibrium in a Perfectly Competitive Market X. Permanent Changes in Market Demand 1) An Increase in Market Demand 2) A Decrease in Market Demand

2/01/2019 · Do You Have Any Firearms – I Dont Answer Questions – Oath Violator Steven G. Ross 129331 – Duration: 19:09. John Filax 11,838,799 views

The generic bread would be supplied under perfect competition, but switching from the generic to the differentiated bread may not change a bakery’s long-run equilibrium output at all.

Chapter 6 Market Equilibrium and the Perfect Competition Model The remaining chapters of this text are devoted to the operations of markets. In economics, a market refers to the collective activity of buyers and sellers for a particular product or service.

The supply curve for a perfectly competitive firm in the short run is the part of the marginal cost curve above the average variable cost curve. S-cool exclusive FREE TUTORIAL offer! Barriers to Entry and Exit Short Run and Long Run Equilibrium

So during the short-run under perfect competition, a firm is in equilibrium in all the above noted situations. We illustrate them diagrammatically as under. Supernormal Profits: The firm will be earning supernormal profits in the short-run when price is higher than the short-run average cost, as shown in Figure 2 (A). The firm is in equilibrium at point E 1 where SMC=MR and SMC cuts MR from

Microeconomics-Chapter-7 Perfect Competition Long Run

Perfect Competition Perfect Competition Long Run And

In a perfectly competitive market in long-run equilibrium, an increase in demand creates economic profit in the short run and induces entry in the long run; a reduction in demand creates economic losses (negative economic profits) in the short run and forces some firms to exit the industry in the long run.

Summary Even though perfect competition is hard to come by, it’s a good starting point to understand market structures. A deep understanding of how competitive markets work and are formed is the cornerstone to understand why it’s so hard to reach them.

true. this is because price is above marginal cost in monopolistic competition whereas price equals marginal cost under perfect competition product variety externality because consumers get some consumer surplus from the introduction of a new product, entry of anew product conveys a positive externality on consumers

The supply curve for a perfectly competitive firm in the short run is the part of the marginal cost curve above the average variable cost curve. S-cool exclusive FREE TUTORIAL offer! Barriers to Entry and Exit Short Run and Long Run Equilibrium

The long-run equilibrium of monopolistic competition is like that of perfect competition in that entry, when the industry makes short-run economic profits, and exit, when it makes short-run economic losses, drives economic profits to zero in the long run.

In perfect competition, market prices reflect complete mobility of resources and freedom of entry and exit, full access to information by all participants, homogeneous products, and the fact that no one buyer or seller, or group of buyers or sellers, has any advantage over another.

Short run equilibrium: – in the short run, the number of firms remains the same. Each firm wants to earn maximum profit. Under monopolistic in the short run, some firms can fix different prices. Keeping in view their total cost, sometimes, new firms earn abnormal profit than others by …

12/06/2011 · Perfect Competition – Short Run Equilibrium In the model of price and output determination under perfectly competitive market conditions, price is determined by the impersonal market forces of supply and demand, and not by individual actions of buyers and sellers.

So during the short-run under perfect competition, a firm is in equilibrium in all the above noted situations. We illustrate them diagrammatically as under. Supernormal Profits: The firm will be earning supernormal profits in the short-run when price is higher than the short-run average cost, as shown in Figure 2 (A). The firm is in equilibrium at point E 1 where SMC=MR and SMC cuts MR from

Monopolistic Competition Emporia State University

Price Determination under Monopolistic Competition M.A

In perfect competition, market prices reflect complete mobility of resources and freedom of entry and exit, full access to information by all participants, homogeneous products, and the fact that no one buyer or seller, or group of buyers or sellers, has any advantage over another.

Perfect Competition – A perfectly competitive –rm is a price taker and faces a horizontal demand curve. Pro–t Maximization – How much should a –rm produce to maximize pro–ts? Competition in the Short Run – What is the market equilibrium when the number of –rms in the market is –xed? Competition in the Long Run – What is the market equilibrium when –rms are free to enter and exit

The long-run equilibrium of monopolistic competition is like that of perfect competition in that entry, when the industry makes short-run economic profits, and exit, when it makes short-run economic losses, drives economic profits to zero in the long run.

The supply curve for a perfectly competitive firm in the short run is the part of the marginal cost curve above the average variable cost curve. S-cool exclusive FREE TUTORIAL offer! Barriers to Entry and Exit Short Run and Long Run Equilibrium

1 Unit 6. Firm behaviour and market structure: perfect competition Learning objectives: to determine short-run and long-run equilibrium, both for the profit-

12/06/2011 · Perfect Competition – Short Run Equilibrium In the model of price and output determination under perfectly competitive market conditions, price is determined by the impersonal market forces of supply and demand, and not by individual actions of buyers and sellers.

Unformatted text preview: Short-Run Equilibrium and Short-Run Supply in Perfect Competition The word “equilibrium” refers to being in a state of rest or balance. You know the meaning of this term in the context of a competitive market: the equilibrium price is the one at which the quantity demanded is equal to the quantity supplied. Neither the buyers nor the sellers have reason to move

ECO 251 Chapter 16 Flashcards Quizlet

Short run equilibrium of a firm under perfect competition

•••We shall now specifically discuss the ‘short-run’ equilibrium of a firm under perfect competition. We assume that the goal of the firm is to earn the maximum profit. Therefore, the point of profit maximisation is the firm’s equilibrium point. By the profit of the firm, we shall mean the profit in excess of normal profit which may also be called the pure profit or the economic

In comparison to perfect competition, the long-run equilibrium in monopolistic competition is characterized by (i) excess capacity. (ii) markup over marginal cost.

2/01/2019 · Do You Have Any Firearms – I Dont Answer Questions – Oath Violator Steven G. Ross 129331 – Duration: 19:09. John Filax 11,838,799 views

true. this is because price is above marginal cost in monopolistic competition whereas price equals marginal cost under perfect competition product variety externality because consumers get some consumer surplus from the introduction of a new product, entry of anew product conveys a positive externality on consumers

Perfect Competition – A perfectly competitive –rm is a price taker and faces a horizontal demand curve. Pro–t Maximization – How much should a –rm produce to maximize pro–ts? Competition in the Short Run – What is the market equilibrium when the number of –rms in the market is –xed? Competition in the Long Run – What is the market equilibrium when –rms are free to enter and exit

CHAPTER 4: PERFECT COMPETITION. LEARNING OBJECTIVE In this topic the principles which guide firms in their price and quantity decisions will be set out in the short and long run. Perfect competition is defined. The demand and marginal revenue are derived. The equivalence between profit maximization and equality of marginal revenue and marginal cost is established. The long run equilibrium …

The generic bread would be supplied under perfect competition, but switching from the generic to the differentiated bread may not change a bakery’s long-run equilibrium output at all.

run equilibrium in a perfectly competitive market, where profit equals zero We observe that the following is the case for a perfectly competitive market in long-run equilibrium:

Under monopolistic competition, the firm will be in equilibrium position when marginal revenue is equal to marginal cost. So long the marginal revenue is greater than marginal cost, the seller will find it profitable to expand his output, and if the MR is less than MC, it is obvious he will reduce his output where the MR is equal to MC. In short run, therefore, the firm will be in equilibrium

12/06/2011 · Perfect Competition – Short Run Equilibrium In the model of price and output determination under perfectly competitive market conditions, price is determined by the impersonal market forces of supply and demand, and not by individual actions of buyers and sellers.

Short run equilibrium: – in the short run, the number of firms remains the same. Each firm wants to earn maximum profit. Under monopolistic in the short run, some firms can fix different prices. Keeping in view their total cost, sometimes, new firms earn abnormal profit than others by …

(3) Under perfect competition price equals marginal cost at the equilibrium output, but under monopoly equilibrium price is greater than marginal cost. Under perfect competition marginal revenue is the same as average revenue at all levels of output. Thus at the equilibrium position under perfect competition marginal cost not only equals marginal revenue but also average revenue.

The supply curve for a perfectly competitive firm in the short run is the part of the marginal cost curve above the average variable cost curve. S-cool exclusive FREE TUTORIAL offer! Barriers to Entry and Exit Short Run and Long Run Equilibrium

(b) Long Run Equilibrium: Under monopolistic competition, the supernormal profit in the long run is disappeared as new firms are entered into the industry. As the new firms are entered into the industry, the demand curve or AR curve will shift to the left, and therefore, the supernormal profit will be competed away and the firms will be earning normal profits. If in the short run firms are

In perfect competition, market prices reflect complete mobility of resources and freedom of entry and exit, full access to information by all participants, homogeneous products, and the fact that no one buyer or seller, or group of buyers or sellers, has any advantage over another.

Short run equilibrium of a firm under perfect competition

Equilibrium of a Firm Under Monopolistic Competition

Perfect, or pure, competition is a market structure char- acterized by (1) a large number of small firms, (2) a homogeneous product, and (3) very easy entry into or exit from the market.

Market Structures and Perfect Competition in the Short Run 8.1 Under Perfect Competition (PC), a market is composed of many firms producing identical products, with no barriers to entry.

12/06/2011 · Perfect Competition – Short Run Equilibrium In the model of price and output determination under perfectly competitive market conditions, price is determined by the impersonal market forces of supply and demand, and not by individual actions of buyers and sellers.

run equilibrium in a perfectly competitive market, where profit equals zero We observe that the following is the case for a perfectly competitive market in long-run equilibrium:

Monopolistic competition – where the short run equilibrium is different to the long run equilibrium Monopoly – advantages and disadvantages. This entry was posted in monopoly .

Under monopolistic competition, the firm will be in equilibrium position when marginal revenue is equal to marginal cost. So long the marginal revenue is greater than marginal cost, the seller will find it profitable to expand his output, and if the MR is less than MC, it is obvious he will reduce his output where the MR is equal to MC. In short run, therefore, the firm will be in equilibrium

3 © 2007 Thomson South-Western Figure 1 Monopolistic Competitors in the Short Run Demand 0 Quantity Price Price Loss-minimizing quantity Average total cost

Short Run Equilibrium Price and Output Under Monopoly

Maximising Consumer Surplus and Producer Surplus How do

Revenue for the Firm V. Short Run Equilibrium – Profit Maximization VI. Graphically A. A Profit B. A Loss C. Breaking even VII. The Shutdown Rule VIII. The Firm’s Short Run Supply Curve IX. Long-Run Equilibrium in a Perfectly Competitive Market X. Permanent Changes in Market Demand 1) An Increase in Market Demand 2) A Decrease in Market Demand

Unformatted text preview: Short-Run Equilibrium and Short-Run Supply in Perfect Competition The word “equilibrium” refers to being in a state of rest or balance. You know the meaning of this term in the context of a competitive market: the equilibrium price is the one at which the quantity demanded is equal to the quantity supplied. Neither the buyers nor the sellers have reason to move

Market Structures and Perfect Competition in the Short Run 8.1 Under Perfect Competition (PC), a market is composed of many firms producing identical products, with no barriers to entry.

2/01/2019 · Do You Have Any Firearms – I Dont Answer Questions – Oath Violator Steven G. Ross 129331 – Duration: 19:09. John Filax 11,838,799 views

CHAPTER 4: PERFECT COMPETITION. LEARNING OBJECTIVE In this topic the principles which guide firms in their price and quantity decisions will be set out in the short and long run. Perfect competition is defined. The demand and marginal revenue are derived. The equivalence between profit maximization and equality of marginal revenue and marginal cost is established. The long run equilibrium …

1/19 Chapter 27: Theory of the firm – perfect competition (1.5) Assumptions of the perfectly competitive market model The firm as a price taker and short run profit maximiser

Monopolistic competition – where the short run equilibrium is different to the long run equilibrium Monopoly – advantages and disadvantages. This entry was posted in monopoly .

run equilibrium in a perfectly competitive market, where profit equals zero We observe that the following is the case for a perfectly competitive market in long-run equilibrium:

Equilibrium of a Firm Under Monopolistic Competition

Short Run Equilibrium of Firm under Perfect Competition

In comparison to perfect competition, the long-run equilibrium in monopolistic competition is characterized by (i) excess capacity. (ii) markup over marginal cost.

Short run equilibrium: – in the short run, the number of firms remains the same. Each firm wants to earn maximum profit. Under monopolistic in the short run, some firms can fix different prices. Keeping in view their total cost, sometimes, new firms earn abnormal profit than others by …

1 Unit 6. Firm behaviour and market structure: perfect competition Learning objectives: to determine short-run and long-run equilibrium, both for the profit-

So during the short-run under perfect competition, a firm is in equilibrium in all the above noted situations. We illustrate them diagrammatically as under. Supernormal Profits: The firm will be earning supernormal profits in the short-run when price is higher than the short-run average cost, as shown in Figure 2 (A). The firm is in equilibrium at point E 1 where SMC=MR and SMC cuts MR from

Equilibrium of a Firm Under Monopolistic Competition

Microeconomics-Chapter-7 Perfect Competition Long Run

(3) Under perfect competition price equals marginal cost at the equilibrium output, but under monopoly equilibrium price is greater than marginal cost. Under perfect competition marginal revenue is the same as average revenue at all levels of output. Thus at the equilibrium position under perfect competition marginal cost not only equals marginal revenue but also average revenue.

true. this is because price is above marginal cost in monopolistic competition whereas price equals marginal cost under perfect competition product variety externality because consumers get some consumer surplus from the introduction of a new product, entry of anew product conveys a positive externality on consumers

3 © 2007 Thomson South-Western Figure 1 Monopolistic Competitors in the Short Run Demand 0 Quantity Price Price Loss-minimizing quantity Average total cost

The supply curve for a perfectly competitive firm in the short run is the part of the marginal cost curve above the average variable cost curve. S-cool exclusive FREE TUTORIAL offer! Barriers to Entry and Exit Short Run and Long Run Equilibrium

1 Unit 6. Firm behaviour and market structure: perfect competition Learning objectives: to determine short-run and long-run equilibrium, both for the profit-

•••We shall now specifically discuss the ‘short-run’ equilibrium of a firm under perfect competition. We assume that the goal of the firm is to earn the maximum profit. Therefore, the point of profit maximisation is the firm’s equilibrium point. By the profit of the firm, we shall mean the profit in excess of normal profit which may also be called the pure profit or the economic

(Figure: A Perfectly Competitive Firm in the Short Run) If market price is G. C) In the long run. 27. In the short run. 0 C) . economic profits are positive. B) The existence of profits leads firms to exit the industry. while losses lead firms to enter the industry. B) …

In a perfectly competitive market in long-run equilibrium, an increase in demand creates economic profit in the short run and induces entry in the long run; a reduction in demand creates economic losses (negative economic profits) in the short run and forces some firms to exit the industry in the long run.

2/01/2019 · Do You Have Any Firearms – I Dont Answer Questions – Oath Violator Steven G. Ross 129331 – Duration: 19:09. John Filax 11,838,799 views

Short run competitive equilibrium in an economy with production Definition A short run competitive equilibrium is a situation in which, given the firms in the market, the price is such that that total amount the firms wish to supply is equal to the total amount the consumers wish to demand.

In comparison to perfect competition, the long-run equilibrium in monopolistic competition is characterized by (i) excess capacity. (ii) markup over marginal cost.

Short run competitive equilibrium U of T Economics

Perfect Competition Economic Efficiency tutor2u Economics

Market Structures and Perfect Competition in the Short Run 8.1 Under Perfect Competition (PC), a market is composed of many firms producing identical products, with no barriers to entry.

Short run equilibrium: – in the short run, the number of firms remains the same. Each firm wants to earn maximum profit. Under monopolistic in the short run, some firms can fix different prices. Keeping in view their total cost, sometimes, new firms earn abnormal profit than others by …

Perfect, or pure, competition is a market structure char- acterized by (1) a large number of small firms, (2) a homogeneous product, and (3) very easy entry into or exit from the market.

So during the short-run under perfect competition, a firm is in equilibrium in all the above noted situations. We illustrate them diagrammatically as under. Supernormal Profits: The firm will be earning supernormal profits in the short-run when price is higher than the short-run average cost, as shown in Figure 2 (A). The firm is in equilibrium at point E 1 where SMC=MR and SMC cuts MR from

Monopolistic competition – where the short run equilibrium is different to the long run equilibrium Monopoly – advantages and disadvantages. This entry was posted in monopoly .

Chapter 6 Market Equilibrium and the Perfect Competition Model The remaining chapters of this text are devoted to the operations of markets. In economics, a market refers to the collective activity of buyers and sellers for a particular product or service.

The long-run equilibrium of monopolistic competition is like that of perfect competition in that entry, when the industry makes short-run economic profits, and exit, when it makes short-run economic losses, drives economic profits to zero in the long run.

Summary Even though perfect competition is hard to come by, it’s a good starting point to understand market structures. A deep understanding of how competitive markets work and are formed is the cornerstone to understand why it’s so hard to reach them.

Perfect Competition – A perfectly competitive –rm is a price taker and faces a horizontal demand curve. Pro–t Maximization – How much should a –rm produce to maximize pro–ts? Competition in the Short Run – What is the market equilibrium when the number of –rms in the market is –xed? Competition in the Long Run – What is the market equilibrium when –rms are free to enter and exit

run equilibrium in a perfectly competitive market, where profit equals zero We observe that the following is the case for a perfectly competitive market in long-run equilibrium:

2/01/2019 · Do You Have Any Firearms – I Dont Answer Questions – Oath Violator Steven G. Ross 129331 – Duration: 19:09. John Filax 11,838,799 views

This paper is about equilibrium under monopolistic competition, incorporating the idea that each seller in such a market must have unique, product-specialized inputs whose uniqueness allows them to earn rent, even in long-run equilibrium.

3 © 2007 Thomson South-Western Figure 1 Monopolistic Competitors in the Short Run Demand 0 Quantity Price Price Loss-minimizing quantity Average total cost

(3) Under perfect competition price equals marginal cost at the equilibrium output, but under monopoly equilibrium price is greater than marginal cost. Under perfect competition marginal revenue is the same as average revenue at all levels of output. Thus at the equilibrium position under perfect competition marginal cost not only equals marginal revenue but also average revenue.

Short Run Equilibrium Price and Output Under Monopoly

Unit 6. Firm behaviour and market structure perfect

This paper is about equilibrium under monopolistic competition, incorporating the idea that each seller in such a market must have unique, product-specialized inputs whose uniqueness allows them to earn rent, even in long-run equilibrium.

In perfect competition, market prices reflect complete mobility of resources and freedom of entry and exit, full access to information by all participants, homogeneous products, and the fact that no one buyer or seller, or group of buyers or sellers, has any advantage over another.

12/06/2011 · Perfect Competition – Short Run Equilibrium In the model of price and output determination under perfectly competitive market conditions, price is determined by the impersonal market forces of supply and demand, and not by individual actions of buyers and sellers.

In a perfectly competitive market in long-run equilibrium, an increase in demand creates economic profit in the short run and induces entry in the long run; a reduction in demand creates economic losses (negative economic profits) in the short run and forces some firms to exit the industry in the long run.

Revenue for the Firm V. Short Run Equilibrium – Profit Maximization VI. Graphically A. A Profit B. A Loss C. Breaking even VII. The Shutdown Rule VIII. The Firm’s Short Run Supply Curve IX. Long-Run Equilibrium in a Perfectly Competitive Market X. Permanent Changes in Market Demand 1) An Increase in Market Demand 2) A Decrease in Market Demand

Perfect Competition – A perfectly competitive –rm is a price taker and faces a horizontal demand curve. Pro–t Maximization – How much should a –rm produce to maximize pro–ts? Competition in the Short Run – What is the market equilibrium when the number of –rms in the market is –xed? Competition in the Long Run – What is the market equilibrium when –rms are free to enter and exit

Equilibrium of a Firm Under Monopolistic Competition

Short run competitive equilibrium U of T Economics

Short run equilibrium: – in the short run, the number of firms remains the same. Each firm wants to earn maximum profit. Under monopolistic in the short run, some firms can fix different prices. Keeping in view their total cost, sometimes, new firms earn abnormal profit than others by …

Perfect Competition – A perfectly competitive –rm is a price taker and faces a horizontal demand curve. Pro–t Maximization – How much should a –rm produce to maximize pro–ts? Competition in the Short Run – What is the market equilibrium when the number of –rms in the market is –xed? Competition in the Long Run – What is the market equilibrium when –rms are free to enter and exit

So during the short-run under perfect competition, a firm is in equilibrium in all the above noted situations. We illustrate them diagrammatically as under. Supernormal Profits: The firm will be earning supernormal profits in the short-run when price is higher than the short-run average cost, as shown in Figure 2 (A). The firm is in equilibrium at point E 1 where SMC=MR and SMC cuts MR from

run equilibrium in a perfectly competitive market, where profit equals zero We observe that the following is the case for a perfectly competitive market in long-run equilibrium:

Short run competitive equilibrium in an economy with production Definition A short run competitive equilibrium is a situation in which, given the firms in the market, the price is such that that total amount the firms wish to supply is equal to the total amount the consumers wish to demand.

Revenue for the Firm V. Short Run Equilibrium – Profit Maximization VI. Graphically A. A Profit B. A Loss C. Breaking even VII. The Shutdown Rule VIII. The Firm’s Short Run Supply Curve IX. Long-Run Equilibrium in a Perfectly Competitive Market X. Permanent Changes in Market Demand 1) An Increase in Market Demand 2) A Decrease in Market Demand

(Figure: A Perfectly Competitive Firm in the Short Run) If market price is G. C) In the long run. 27. In the short run. 0 C) . economic profits are positive. B) The existence of profits leads firms to exit the industry. while losses lead firms to enter the industry. B) …

This paper is about equilibrium under monopolistic competition, incorporating the idea that each seller in such a market must have unique, product-specialized inputs whose uniqueness allows them to earn rent, even in long-run equilibrium.

Suppose that demand for a product increases from D1 to D2 In the short run, price rises from Po to P 1; super-profits are made, firms are attracted into the industry and the supply curve will therefore shift out.

Supply in a Competitive Market University of Southern

Monopolistic Competition Emporia State University

true. this is because price is above marginal cost in monopolistic competition whereas price equals marginal cost under perfect competition product variety externality because consumers get some consumer surplus from the introduction of a new product, entry of anew product conveys a positive externality on consumers

12/06/2011 · Perfect Competition – Short Run Equilibrium In the model of price and output determination under perfectly competitive market conditions, price is determined by the impersonal market forces of supply and demand, and not by individual actions of buyers and sellers.

1/19 Chapter 27: Theory of the firm – perfect competition (1.5) Assumptions of the perfectly competitive market model The firm as a price taker and short run profit maximiser

The generic bread would be supplied under perfect competition, but switching from the generic to the differentiated bread may not change a bakery’s long-run equilibrium output at all.

In comparison to perfect competition, the long-run equilibrium in monopolistic competition is characterized by (i) excess capacity. (ii) markup over marginal cost.

•••We shall now specifically discuss the ‘short-run’ equilibrium of a firm under perfect competition. We assume that the goal of the firm is to earn the maximum profit. Therefore, the point of profit maximisation is the firm’s equilibrium point. By the profit of the firm, we shall mean the profit in excess of normal profit which may also be called the pure profit or the economic

So during the short-run under perfect competition, a firm is in equilibrium in all the above noted situations. We illustrate them diagrammatically as under. Supernormal Profits: The firm will be earning supernormal profits in the short-run when price is higher than the short-run average cost, as shown in Figure 2 (A). The firm is in equilibrium at point E 1 where SMC=MR and SMC cuts MR from

(c) Short Run Equilibrium With Losses Under Monopoly: A monopolist also accepts short run losses provided the variable costs of the firm are fully covered. The loss minimizing short run equilibrium analysis is presented graphically.

3 © 2007 Thomson South-Western Figure 1 Monopolistic Competitors in the Short Run Demand 0 Quantity Price Price Loss-minimizing quantity Average total cost

Monopolistic competition – where the short run equilibrium is different to the long run equilibrium Monopoly – advantages and disadvantages. This entry was posted in monopoly .

In a perfectly competitive market in long-run equilibrium, an increase in demand creates economic profit in the short run and induces entry in the long run; a reduction in demand creates economic losses (negative economic profits) in the short run and forces some firms to exit the industry in the long run.

The supply curve for a perfectly competitive firm in the short run is the part of the marginal cost curve above the average variable cost curve. S-cool exclusive FREE TUTORIAL offer! Barriers to Entry and Exit Short Run and Long Run Equilibrium

Perfect, or pure, competition is a market structure char- acterized by (1) a large number of small firms, (2) a homogeneous product, and (3) very easy entry into or exit from the market.

Perfect Competition – A perfectly competitive –rm is a price taker and faces a horizontal demand curve. Pro–t Maximization – How much should a –rm produce to maximize pro–ts? Competition in the Short Run – What is the market equilibrium when the number of –rms in the market is –xed? Competition in the Long Run – What is the market equilibrium when –rms are free to enter and exit

In perfect competition, market prices reflect complete mobility of resources and freedom of entry and exit, full access to information by all participants, homogeneous products, and the fact that no one buyer or seller, or group of buyers or sellers, has any advantage over another.

Microeconomics Perfect Competition

Short run competitive equilibrium U of T Economics

Short run competitive equilibrium in an economy with production Definition A short run competitive equilibrium is a situation in which, given the firms in the market, the price is such that that total amount the firms wish to supply is equal to the total amount the consumers wish to demand.

Perfect, or pure, competition is a market structure char- acterized by (1) a large number of small firms, (2) a homogeneous product, and (3) very easy entry into or exit from the market.

Short run equilibrium: – in the short run, the number of firms remains the same. Each firm wants to earn maximum profit. Under monopolistic in the short run, some firms can fix different prices. Keeping in view their total cost, sometimes, new firms earn abnormal profit than others by …

In comparison to perfect competition, the long-run equilibrium in monopolistic competition is characterized by (i) excess capacity. (ii) markup over marginal cost.

12/06/2011 · Perfect Competition – Short Run Equilibrium In the model of price and output determination under perfectly competitive market conditions, price is determined by the impersonal market forces of supply and demand, and not by individual actions of buyers and sellers.

true. this is because price is above marginal cost in monopolistic competition whereas price equals marginal cost under perfect competition product variety externality because consumers get some consumer surplus from the introduction of a new product, entry of anew product conveys a positive externality on consumers

(c) Short Run Equilibrium With Losses Under Monopoly: A monopolist also accepts short run losses provided the variable costs of the firm are fully covered. The loss minimizing short run equilibrium analysis is presented graphically.

The long-run equilibrium of monopolistic competition is like that of perfect competition in that entry, when the industry makes short-run economic profits, and exit, when it makes short-run economic losses, drives economic profits to zero in the long run.

(Figure: A Perfectly Competitive Firm in the Short Run) If market price is G. C) In the long run. 27. In the short run. 0 C) . economic profits are positive. B) The existence of profits leads firms to exit the industry. while losses lead firms to enter the industry. B) …

Nelson Education Exploring Microeconomics Second

Price-output determination in monopolistic competition

2/01/2019 · Do You Have Any Firearms – I Dont Answer Questions – Oath Violator Steven G. Ross 129331 – Duration: 19:09. John Filax 11,838,799 views

Under monopolistic competition, the firm will be in equilibrium position when marginal revenue is equal to marginal cost. So long the marginal revenue is greater than marginal cost, the seller will find it profitable to expand his output, and if the MR is less than MC, it is obvious he will reduce his output where the MR is equal to MC. In short run, therefore, the firm will be in equilibrium

The long-run equilibrium of monopolistic competition is like that of perfect competition in that entry, when the industry makes short-run economic profits, and exit, when it makes short-run economic losses, drives economic profits to zero in the long run.

3 © 2007 Thomson South-Western Figure 1 Monopolistic Competitors in the Short Run Demand 0 Quantity Price Price Loss-minimizing quantity Average total cost

true. this is because price is above marginal cost in monopolistic competition whereas price equals marginal cost under perfect competition product variety externality because consumers get some consumer surplus from the introduction of a new product, entry of anew product conveys a positive externality on consumers

Summary Even though perfect competition is hard to come by, it’s a good starting point to understand market structures. A deep understanding of how competitive markets work and are formed is the cornerstone to understand why it’s so hard to reach them.